Tax cut proposal Despite Trump’s tax cut announcement for individuals earning under $200,000 through tariff revenue on Sunday, he also repeatedly ruled out the millionaire’s tax. Yet, the problem lingers in the potential consumption deficit. Most low- to medium-income earners mainly spend their income on necessary goods rather than taxes, so raising the tariffs will only result in higher costs and will continue to burden purchasing power. This will lead to degrowth in response unless domestic production comes in. China While the market awaits the trade progress between the US and China, no recent US-China talks have occurred yet. In fact, China’s Foreign Minister Wang Yi emphasized strengthening BRICS influence with Russia, which could potentially challenge the U.S. dollar’s dominance and further intensify the trade tension. Russia-Ukraine Ceasefire Russia’s Putin declared a temporary ceasefire for the May holidays, and the White House reports Trump’s push for a permanent Russia-Ukraine ceasefire. Both the US and Ukraine are eager to end this as soon as possible. Nuclear Talk Israel’s Ron Dermer expressed confidence in Trump’s firm stance against a weak Iran nuclear deal, with Iran proposing nuclear talks in Rome on May 2 with France, Britain, and Germany. Looking Forward: JOLTs Job Openings will offer labor market conditions in the United States, which also detail the number of job openings, separations, and hiring activities.

Weekly Data Summary Report As of April 26, 2024

Weekly Data Summary Report As of April 26, 2024 Below is the two-week summary on the major economies such as the United States, the Eurozone, and Japan, which is mainly based on the economic indicators, critical events related to President Donald Trump’s trade conflict with other trading partners, and gold price movements. Disclaimer: Please note this is opinion-based; do not take it as investment advice. The United States The US economy experienced significant volatility due to the escalation of the trade war and policy uncertainty. The period began with rising US-China trade tensions and Trump’s attacks on Federal Reserve Chair Jerome Powell for refusing to lower the rate. These attacks fueled market anxiety and sparked gold prices to a record high of $3,500 per ounce on April 22, 2025, before pulling back slightly to $3,281.60 on April 23 as tariff de-escalation hopes grew. In fact, Trump softened his stance toward both China’s trade conflict and Powell, citing on lowering of tariffs on China’s goods while backing off his threat to fire FED Chair Powell. With these two main events this week, we could assume that the recent market was marked by trade-driven factors that fueled market swings, consumer sentiment, and gold price volatility. Therefore, any signals of potential US-China trade easing would continue to temper the gold prices amid persistent uncertainty. One thing to remember is that if tension sparked once again while Trump has the power to threaten to lower the interest rate, then this would also push the gold back to its peak. As of now, as per the CME FEDWatch tool, the market is still priced in for a rate hold until June 2025. Looking forward: The US employment report this week will also cause huge volatility and offer further insights about the labor market conditions. The Eurozone After Trump’s 90-day suspension of 20% tariffs, no agreement materialized until today. Yet, as Moody’s has flagged, the Eurozone economy is still facing the risk of recession. With a downgraded outlook from major unions such as Germany, France, Italy, and Spain, this suggests that the EU is still experiencing stagnation, particularly in the manufacturing and services sectors, while external demand remains weak amid tariff tensions. Therefore, the market anticipates further easing in April to boost growth, although inflation and supply chain disruption could be challenges. Japan Although not much changes for Japan’s economy this week, Japan is still facing stagnation risk from Trump’s tariffs, particularly in its auto and export sectors, which could potentially cut the growth forecast. In fact, the IMF cut Japan’s growth forecast from 1.1% to 0.6%. This is a result of Japan’s dependent market in China after its first trading partner, the US, so changes between Trump and China could also affect Japan’s market. Therefore, all eyes are on the Bank of Japan’s interest rate decision, which takes place this week with an unchanged rate. But the important part falls on the speeches and statements that could dictate further economic insights.

Trump’s Economic Optimism Meets Federal Reserve Caution

President Donald Trump President Donald Trump acknowledged that his tariff policies might lead to some “transition challenges” but remained optimistic about their success. This follows the White House’s announcement that U.S. tariffs on China have increased to 145%. Trump is also pushing for a major tax cut package and a debt ceiling hike. The proposed budget includes up to $5.3 trillion in tax reductions over ten years and raises the debt ceiling by $5 trillion in exchange for $4 billion in spending cuts. Federal Reserve Despite having a lower inflation reading, several Federal Reserve members from last night further emphasized the inflation problem while addressing that the risk of a higher unemployment rate and slower growth would come if the tariff overshoots the expected. And that could lead to a delay in rate cuts this year, as per Federal Reserve Bank of Boston President Susan Collins.

125% tariff on China, 10% or 90 Days pause for the Rest: Markets Cheer Now, Brace for Later

A piece of positive news for the stock market last night came when President Trump paused on big tariffs on countries except for China. Trump raised China’s tariff to 125% and lowered reciprocal tariffs to 10%; both are effective immediately. As for non-retaliating countries, they will be authorized with a 90-day pause. Given how the strong statement has already accelerated the stock prices positively, Fear index dropped while putting some downward pressure on the GOLD price for a short period. this reflects how the market became more certain—at least for the next 90 days. The dip and then surge in gold prices to $3,117 per ounce as we speak, also interpreted as a growing confidence in the safe-haven assets followed by a rebound as longer-term uncertainties remain. So here is the catch: All are positive for the stock market, the US economy, and everyone! My thought → I believe Trump’s intention was to use an aggressive tariff to pull some cold water on the stock market, with the purpose of forcing some reliant exported-company stock to decline and seek back to US production. That is also another reason why he mentioned last time not looking at the stock market, let alone the downfall in recent days. All will help to support their in-house production goal, just as he always repeated in his remark. While this also could be another way of forcing the FED to lower the interest rate with a risk of recession from every corner. Now, things have final Forward-Looking: The Consumer Price Index, released tonight, is a key highlight of the week, offering valuable insights into how pricing has shifted as some of Trump’s policies have finally taken effect.

Trump Escalates Tariff War with China, Signals Broader Trade and Energy Policy Shifts

President Trump intensified the U.S.-China trade war, announcing a 104% tariff on Chinese goods, which will take effect April 9 at 12:01 AM ET, while China vowed to “fight till the end” and filed a WTO dispute against the U.S. reciprocal tariff. China is also willing to strengthen political mutual trust with the EU and India. All of these are signaling a deepening trade war with major trading partners. U.S. Trade Representative Greer defended the aggressive tariff strategy, stating that companies heavily reliant on imports from China and Asia will face pricing challenges. Furthermore, he also dismissed concerns about inflation, while Trump has also made it clear that no tariff exemptions will be granted in the near term, according to Greer. Especially when Trump already signaled that he will bring discussion on foreign aid and the US military presence for a better trade negotiation. As a matter of fact, Trump believes that the US will be able to make in-house iPhones. Existing Tariff on Cars, Lumber, and Steel Trump highlighted the effects of existing tariffs on cars, lumber, and steel as he claimed that this would accelerate US domestic manufacturing/production. Other than this, he is also pledging unwavering support for the coal industry, citing that “We will give a guarantee the coal business can’t be terminated” while announcing billions of dollars of investment for next-generation coal technology. For now, what we are seeing is that both Trump and China show no signs of backing down, which could prolong the slowdown.

Trade Wars and Market Woes: Trump’s Moves Rattle the Globe

Global stock markets plummeted for a third consecutive session on Monday, with European and Asian markets posting sharp declines following the latest U.S. tariff announcements. The commodities market also took a hit, with gold dropping to a new low of $2,957 per ounce this week. Here’s a breakdown: Japan’s Response to Trump’s Trade Policies Japan has strongly warned about Trump’s tariff negatively impacting the global economy and free trade system while stating that “Japan will not sacrifice its domestic industries just to appease Trump.” Despite these tensions, Trump described a recent call with Ishiba as highly productive, suggesting optimism amid the standoff. U.S.-EU Trade Tensions President Trump pressed the European Union to buy more U.S. energy to reduce the trade deficit, dismissing the EU’s current tariff response as “not enough.” While the EU commission responds with a potential 25% tariff on US goods, which will take effect from May 16th. U.S.-China Trade Conflict Escalates Meanwhile, Trump escalated tensions with China, threatening an additional 50% tariff on Chinese goods if China does not retract its recent 34% tariff increase by April 8, 2025. The new U.S. 50% tariffs will begin on April 9. U.S.-Iran Nuclear Tensions Trump has taken a firm stance against Iran possessing nuclear weapons and warned of severe consequences if talks fail. He hinted at a potential direct meeting with Iran on Saturday, though details remain unconfirmed. U.S. Economic Policy Outlook

Weekly Data Summary Report as of April 05, 2025

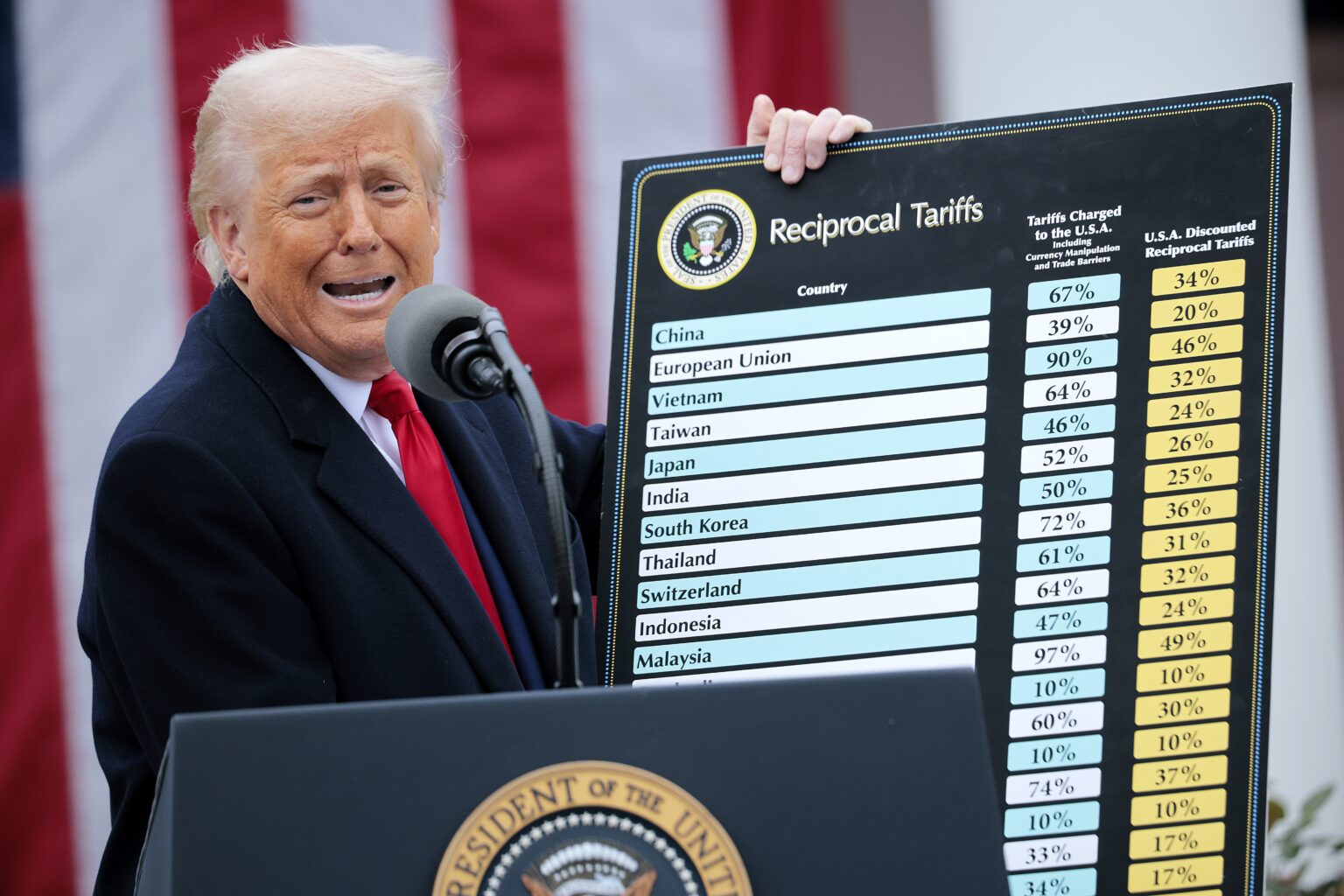

Weekly Data Summary Report As of April 05, 2024 In this report, we will assess major economies, including the United States, the United Kingdom, the Eurozone, and China, mainly based on their economic indicators and economic events that have occurred within this week. The United States Last week, the market was more focused on Trump’s tariff escalation, rising recession fears, and persistent inflation pressures than on the data itself. This led to a plummet in the US stock market and significant volatility in the commodities market. On “Liberation Day,” Trump declared a universal 10% tariff on imports on April 05, while higher reciprocal tariffs—such as 54% on China, 20% on the European Union, 49% on Cambodia, and many more—were set to begin April 9. Not only were the major trading partners being affected, but even small countries also faced the same problem. All are raising the bar on recession, and fear led the investor to leave the market, resulting in lower liquidity in the market, which pushes to higher volatility in the market—stocks dumped, US 10-year yield down, GOLD prices down, and VIX up. These showed that uncertainty is rising to the point (fear over greed) that gold and other asset classes have become less attractive to investors. As shown in our previous post, we also mentioned that fear overtakes greed. Therefore, what we can monitor from now is when the stock market opens. Is Jim Cramer’s warning about Black Monday coming true? Taking a step back on the data release, the majority are supporting higher inflation pressure, while the business activities are scaling back most negatively. While some labor data gave a mixed picture, we also see layoffs starting to mount and slow hiring activities in industries, particularly in retail and manufacturing reliant on imports. Even Powell and experts from investment banks are also citing a possibility of a recession while the markets are pricing in the FED Fund rate cut earlier, to June this year. In short, mixed labor market conditions + higher inflation + weak economic growth + tariff tensions → higher uncertainty in the market → stocks plunged last week and might continue to do so. The United Kingdom For the UK economy, the 10% tariffs came on top of the existing 25% tariffs on steel, aluminum, and automobiles, which have led many UK stocks to slump further due to fears of a global trade war escalating. Although the UK avoided the higher reciprocal tariffs, many businesses still worried over the potential external shock that might influence higher pricing and slower demand. Even the National Institute of Economic and Social Research (NIESR) also forecasts near-zero economic growth in 2025 if this tension escalates. One thing is for sure: inflation will surely eat up everyone’s purchasing power unless Trump achieves the zero-trade policy. The European Meanwhile, the Europeans also faced the same problem with a tumbling stock market and a decline in growth forecasts amid higher inflation. With a fragile economic outlook skewing around the recession risk, Goldman Sachs has already expected a 0.7% GDP reduction by the end of 2025, while the European Central Bank (ECB) is anticipating slower growth at 0.1% in Q2, 0% in Q3, and 0.2% in Q4. Therefore, they projected a potential rate cut in April and June. → My concerns fall on the German economy, which is export-oriented and reliant on the manufacturing sectors. With ongoing trade tension, this economy will be affected the most, with a possibility of recession looming. China After Trump announced a 54% tariff on China on April 04, China struck back with a 34% tariff on all US imports effective April 10, alongside a WTO complaint and export controls on rare earths like samarium, gadolinium, and dysprosium—critical for U.S. tech and defense industries. This has led the US-China trade war to escalate while dipping both Chinese stocks and US stocks even further as uncertainty arose.

Trump’s Tariff Bombshell: 10% Base Rate Hits April 5, Targeted Hikes Loom as Markets Brace for Stagflation

President Donald Trump’s early morning tariff announcement brought a flood of details, so let’s break it down. Now, the market is panicking due to stagflation fear and global uncertainty that stemmed from earlier this morning. Experts from Markets Live, Macro Strategist, JPMorgan Asset Management, Goldman Sachs, Bank of America Corp., and others expressed their concerns on the tariff problem that could deepen equity sell-offs and push the economy toward stagflation. The responses from major trading partners are incoming and will be the highlight of the month; therefore, the old playbook still applies. If these partners retaliate, the risk of stagflation will grow, keeping markets on edge. If fear overtakes greed and investors flee, we could see a wave of sell-offs. Market Reaction: Gold prices rally above $3160 per ounce as Trump’s tariff news amplifies stagflation worries and market uncertainty.

Will Trump’s third tariff option ease some tension in the market?

Major central banks, either from the Federal Reserve, the Bank of Japan, or even others, continue to stress the impact of the US tariffs on the respective nations, namely in the inflation problem. Even in the Purchasing Managers’ Index report from ISM last night, the business survey also worried that this import inflation would scale back on their profit margin and long-term prospects of their business operation. Pricing soared to 69.4, the highest since mid-2022, which also marks a year of inflation coming back. The pain point is that weak labor markets and demand are coming into play, which could paint a picture of overall deterioration in the manufacturing sector. And again, not only in the US! A familiar source from WSJ reported that President Donald Trump’s economic team is preparing a third tariff option that could be less than a 20% tariff on a subset of nations. If this third tariff option signals a more targeted but still disruptive trade policy while raising more trade disputes with China, demand for gold could rise, pushing prices upward. And vice versa, if this third option hints at easing the uncertainty through lowering the tariff on major trading partners. For now, Israel eliminated the tariff on US-imported goods, leading to a positive sign for everyone, while Canada and Mexico are ready for a reciprocal tariff if Trump decides to pursue this so-called reciprocal tariff. According to the White House, the car tariffs go into effect on April 3rd, while repeating the claims that everyone can avoid the tariff by moving production to the US.

Is Gold Eyeing $3,200 This Month?

As of April 01, gold hit a record high above $3,130 per ounce, fueled by tariff anticipation, inflation fears, and safe-haven demand—setting the stage for April. Here is something you should look forward to in April. ***Disclaimer: This content reflects personal opinions and is intended for informational purposes only. It should not be construed as financial advice. Consult with a qualified financial advisor before making any investment decisions. Thank you. Fundamental Analysis Factor 1: Reciprocal Tariff Date or Liberation Day (Main Event)Trump’s pledge to impose reciprocal tariffs on neighboring countries, particularly in China, the EU, and possibly Russia, as well as nations reliant on Venezuela’s oil exports. And any further escalation could increase market uncertainty Remember: Highlight: Trade tensions rising would lead to inflation fear and uncertainty, which potentially boosts gold as a hedge. Factor 2: Escalating WarMilitary threats over Iran’s nuclear program if an agreement is not reached, along with Middle East flare-ups, are all heightening uncertainty and boosting gold. Highlight: War tension persists, which would lead investors to risk-off, spiking safe-haven demand further. Factor 3: Federal ReserveThe Fed is planning to slow balance sheet runoff starting April 1, suggesting a view of approaching the quantitative easing (QE) but not entirely. All of this is leading to the devaluation of the US dollar and the pushing of gold even higher. Highlight: A dovish Fed could support gold prices, though exemptions or firm QT might turn it bearish short-term. Technical Analysis Here are some scenarios for the GOLD price in April: